Vessel delays are finally showing some signs of improvement - as are the terminal congestion indicators, according to Sea-Intelligence.

“That said, the congestion situation is still far from normal,” says the maritime consultancy’s CEO Alan Murphy.

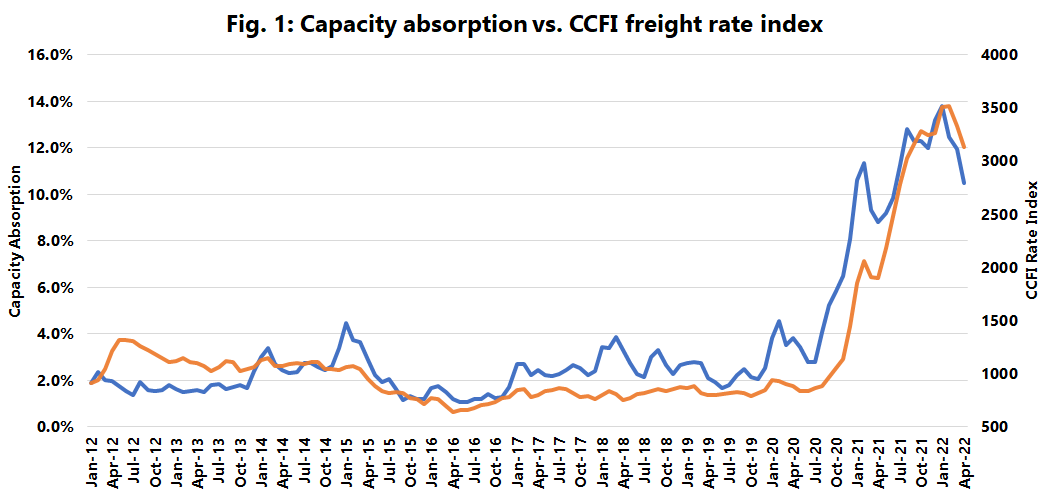

An analysis of the figures shows that while 10.5% of the global fleet is still unavailable due to supply chain delays, it has dropped from 13.8% in January.

“This means that 3.3% of the global fleet was released back into operation from January to April,” says Murphy.

Figure 1 shows that CCFI (China Containerised Freight Index) freight rates are highly correlated with the capacity absorption rate, clearly showing how this loss of capacity is the most important factor in the ongoing crisis, Murphy explains. “It appears that the capacity absorption has acted as a leading indicator for rate developments since the congestion problems began in earnest during late 2020.”

On terminal congestion, the consultancy has been using the bi-weekly customer advisories from HMM to calculate a terminal congestion index.

In North America, the index has been gradually increasing since reaching an apex of a little over 80% in January, but still remains at a highly elevated level.

“However, what is interesting to note is that in Europe there has been continuing substantial improvement in the overall congestion index over the past month – although it should also be noted that despite the very visible decline, the level of congestion is still very high compared with pre-pandemic normality.

“On a port level, distinct improvements are seen in Spain, Italy, and Greece, whereas at the other end of the scale there is not much improvement in Rotterdam and Hamburg.”