The major shipping lines (that report financial figures) made a staggering $124 billion in operating profit in 2021, following that up with nearly $122bn in the first three quarters of 2022 alone, according to figures just released by maritime consultancy Sea-Intelligence.

Of this, the 2022-Q3 figure stands at $35.6bn so far (minus CMA CGM which has published its Ebitda but not its Ebit/operating profit).

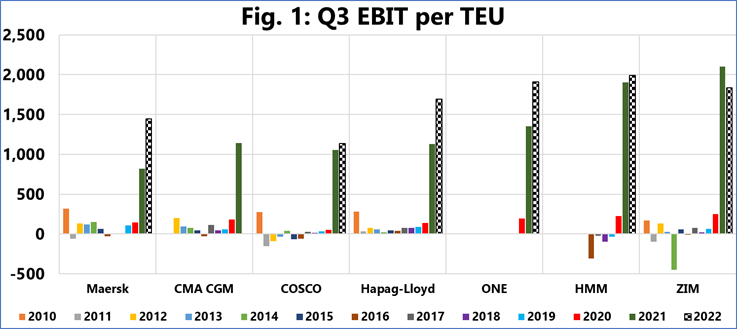

Figure 1 shows the Q3 Ebit/TEU for 2010-2022 for the major carriers that report Ebit and global volumes. The figures for 2021-Q3 and 2022-Q3 dwarf those of the previous years, with some of the carriers seeing a substantial increase year on year (y-o-y) in 2022-Q3. ZIM was the only carrier with a y-o-y decrease, but still with one of the strongest 2022-Q3 Ebit/TEU figures.

However, not all the developments are positive from the perspective of the shipping lines, says Sea-Intelligence CEO Alan Murphy. “While most of the larger carriers recorded double-digit revenue growth y-o-y, the smaller carriers struggled in that respect, which is not surprising given the falling freight rates.

“Same is the case with Ebit; the smaller carriers are struggling to grow their Ebit y-o-y and are recording various levels of decline. The underlying numbers are still strong though, but the data strongly suggests that we are at the end of the line of the carrier profitability boom.”